Automatically fill out an income tax return in 1C 8.3 Accounting 3.0

The user needs to do some “preparatory” work before proceeding with the calculation. It consists of three main stages:

- Setting up the program

- Correct data entry

- Regular operations at the end of the month

Setting up income tax in 1C 8.3

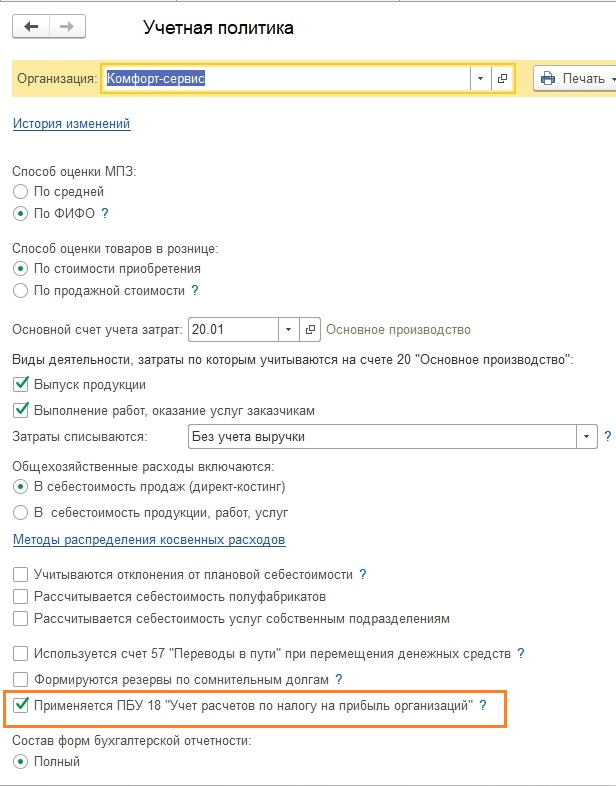

What settings affect the calculation of income tax? First of all, you need to understand the “Income Tax” tab in the accounting policy (Fig. 1).

The “Apply PBU18...” checkbox does not affect the calculation of tax, or rather not the final result, but the display of intermediate data and some important reports. For example, the report “Analysis of income tax accounting” will be generated correctly only if the checkbox is checked, since it takes into account permanent and temporary differences.

Filling out the register “Methods for determining direct production costs in NU” is mandatory for organizations that produce products and provide services (Fig. 2). The initial data is entered automatically, so the user receives a ready-made “fish”, which can later be used for advanced customization to suit his needs.

The principle of filling out is simple: everything that is in this register is considered direct expenses, everything else is indirect. If this register is not filled in, some lines of the Declaration will remain empty.

The directory “Nomenclature Groups” is intended for detailing income - it is for these nomenclature groups that sales income will be displayed in the Declaration (Fig. 3).

- No manual operations

- Relevant analytics of income and expenses

What are the dangers of manual operations? The fact is that each entry in 1C is not only the amounts for the debit and credit of accounting, but also the amounts for tax accounting, including permanent and temporary differences. Differences are calculated automatically using a well-known formula:

BU = NU + PR + VR,

- BU = accounting amount

- NU – tax accounting amount

- ETC. VR – sums of permanent and temporary differences, respectively

It is not always possible to fill out all the amounts correctly manually. Errors arise that take a lot of time to find. For example, in Fig. 4 there is no amount for the tax entry credit. In the future, this will lead to an error in calculations and the Declaration will be formed incorrectly.

Entering data for the declaration

The second rule is that it is important not to make mistakes when filling out income and expense analytics (cost accounts, cost items, item groups, divisions).

For example, in the document “Production Report for a Shift”, the product groups on the “Products” and “Materials” tabs must correspond to each other (Fig. 5), and the cost item must be present in the register “Methods for determining direct production costs of NU”

Formation of a profit declaration in 1C 8.3

And the last stage before the formation of the Declaration is the Closing of the month (Fig. 6).

All regulatory operations must be completed without errors, and for each month of the period of formation of the Declaration. This is a must. In order not to deal with many errors on the last day, it is recommended to carry out preliminary closings of periods several times and correct errors “on-line”.

After closing the month, it is worth checking the balances on account 68.04.2. If everything is correct, the balances on it should be zero (Fig. 7). This account was specially added to 1C for income tax calculations.

Now in 1C Accounting you can create the Declaration itself. It is in the list of regulated reports (Fig. 8).

The magic “Fill” button does all the routine work (Fig. 8). The user remains to check the amounts included in the sections of the Declaration.

It’s logical to start checking from the second sheet, which shows expenses.

There are two verification methods:

- Decoding

- Tax accounting registers

To decrypt, you need to place the cursor on the desired line and press the corresponding button.

Tax accounting registers are located in the “Reports” section (Fig. 10).

Tax registers can be presented to tax authorities during audits to confirm the calculated tax base (Fig. 11).

Similarly, in 1C 8.3 the remaining sections of the declaration are checked.

Before sending the Declaration to the tax office, one more check should be performed (Fig. 12).

Based on materials from: programmist1s.ru

This review is devoted to the procedure for calculating income tax and filling out the corresponding declaration in 1C 8.3, configuration “1C: Enterprise Accounting”. It is assumed that the reader is already familiar with the principles of PBU 18/02. It is impossible to cover the entire Chapter 25 of the Tax Code of the Russian Federation in one article; we will focus on the main points and consider the algorithm of actions for calculating income tax using the 1C program.

The income tax return in 1C reflects income and expenses accepted for calculating the tax base for income tax. The procedure for filling it out is described in detail in the Order of the Federal Tax Service MMV-7-3/572@ dated October 19, 2016.

The tax period for all companies is a calendar year, the deadline for submitting the annual return is March 28. If the last day for submitting the declaration falls on a weekend, it is postponed to the next working day.

There are some nuances regarding reporting periods and advance payments:

Organizations with small turnover submit reports during the year based on the following results:

- 1 quarter until April 28;

- Semester until July 28;

- 9 months until October 28th.

At the same time, payments are made on accrued profits, which are considered advance payments, because The full tax amount will be generated only at the end of the year. Sometimes situations are possible when the amount of advance payments paid during the year exceeds the tax accrued at the end of the year, then the organization has an overpayment of tax.

If the organization’s average quarterly revenue over the last 4 quarters is equal to or exceeds 15 million rubles, then they pay monthly advance payments for income tax by the 28th, formed by calculation (an example of calculation will be later). The deadline for submitting reports is similar to that given in the previous paragraph. If at the end of the quarter the amount of advance payments is less than the amount of actually accrued tax, the delta will have to be paid additionally.

The procedure for making an advance payment of income tax every month is not always beneficial for the organization. There are situations when there is no profit, but you have to pay advances. In this case, the organization can switch to the calculation procedure based on the actual profit received: at the end of each month it will be necessary to submit reports to the tax authorities.

To switch to this regime, you must submit the appropriate application before the start of the calendar year, then you will not be able to change the regime until the end of the tax period.

Income tax in 1C 8.3. Step-by-step instruction

- Fill in the accounting policy settings.

- Fill out reference books related to tax registers. Pay special attention to the expense guide.

- When entering documents, correctly indicate parameters that can affect the calculation of income tax: accounts and subaccounts according to the Chart of Accounts, types of income or expenses, item groups, etc. If the documents contain special settings for tax accounting, you should pay special attention to them and, if necessary, fill out them. When entering a document, you should analyze the transactions and pay attention to the display of data in the NU.

- After entering all the documents for the month, you should generate the regulatory documents Closing the month and check the results. If the results in 1C do not coincide with the expected ones, it means that somewhere in the settings or entered documents an error was made.

- According to Kt. 68.04.1, the correct amount of income tax must be generated for the month. If you have achieved such a situation in 1C, you can go to regulatory reports and create a declaration.

- We generate and check the declaration. Sometimes you don't like the distribution of direct and indirect costs. This can be adjusted with the appropriate settings. If all the items in the declaration correspond to our expectations, we download it and send it to the tax office.

- Next, you should pay the tax and reflect the payment in 1C. Account 68.04.1 should display the real balance, reflecting the accounting for income tax on tax in terms of settlements with the tax inspectorate and budgets.

Let's look at an example of calculating tax for a quarter. The first two months of the example show options for permanent and temporary differences; in the third month we will add the purchase and sale of goods.

How to calculate income tax in 1C

Let's implement the discussed theoretical steps in practice. Let's look at the accounting policy settings. The parameter must be set that we use the eighteenth PBU.

So far the wiring in the control unit and the control unit are the same. But, since the type of expenses indicates normalized advertising expenses, when performing a routine operation to close the month in NU, an amount not exceeding 1% of revenue will be written off as expenses.

It contains non-acceptable expenses that create permanent differences.

We will show the postings for revenue. Every month during the quarter these will be services.

Let's look at the SALT for January. Pay attention to the difference in NU and BU according to our example. On account 26, advertising expenses remained uncovered in NU. In January you can write off only 1 thousand rubles. But if there is revenue next month, you can write off an additional amount. On account 99.02.1 is the amount of conditional income tax expense. Temporary differences affected account postings. 09 and 77. The constant difference was reflected in the account 99.02.3, and the difference in advertising was also added there. On account 68.04.1 is the total amount payable for income tax.

Let's look at account card 68.04.2, which reflects the accrual of income tax. This is a rare case when it is more logical to consider the report from the end of the document. Then the amounts generated from the influence of permanent and temporary differences are added to the conditional income tax expense. The final tax amount is transferred to the account for settlements with the budget, divided into federal and regional payments.

In the second month, operations to write off depreciation in the accounting department for workwear and reduce PNO are added to the already familiar turnover. Additionally, advertising costs are written off to NU, resulting in the amount in the account. 99.02.3 is decreasing.

We create a profit declaration. We fill out the title page, the correction number must be zero. When submitting updated declarations, the adjustment number will be increased. Click the “Fill” button to create the sections of the declaration.

Let's consider those that have data. Section 1 reflects the amount payable by budget. You should check that the KBK is filled out correctly, and then indicate it on the payment slip when paying the tax.

Appendix 02 – breakdown of expenses. For many lines of the declaration, you can see more detailed detail. To do this, select a cell and click the “Decrypt” button.

For example, this is what a breakdown of direct costs looks like.

After filling out the declaration, you can check it, upload it electronically to external media, or send it to the tax office directly from the program.

Let's take a closer look at the calculation of advance payments. The amount of calculated tax for the quarter is 83,640. If an enterprise operates in the mode of paying only quarterly advance payments, it must pay this amount at the end of the 1st quarter by April 28 and quietly work throughout the second quarter, without worrying about payments and profit reporting.

But if the company falls under the criteria for paying monthly estimated advance payments (let such period come on April 1), then 1/3 of this amount, 27880, it will have to pay every month during the second quarter by April 28, May 28 and June 28. Then, at the end of the quarter, calculate the tax amount for the six months and compare it with the advance payments already paid. If you paid less than what was actually accrued, you must pay the difference by July 28.

Advances for the third quarter are calculated as (amount of tax for half a year) minus (amount of tax for the first quarter) and then 1/3 of this value is taken for monthly payments.

Advances for the fourth quarter are calculated in the same way (tax amount for 9 months) minus (tax amount for half a year) and then divided by 3. The resulting amount must be paid monthly in the fourth quarter. And the same amount will be payable in each month of the first quarter of the next year.

As noted above, if an enterprise considers it inappropriate to pay monthly advance payments, it can switch to the mode of payment based on actually received profits, having previously notified the tax authorities about this.

With this, we have completed our consideration of the main points related to the calculation of income tax and the formation of the corresponding declaration in 1C 8.3.

Income tax for payment to the budget is calculated on the basis of Chapter 25 of the Tax Code of the Russian Federation:

Income tax = Taxable income × Income tax rate.

Tax base for calculation income tax in 1C it is defined as the difference between income and expenses, which may differ from those adopted in accounting. In this case, differences arise between profit, and therefore the calculated income tax according to accounting and NU.

The differences that arise between accounting and tax profit (loss) can be of two types: permanent (PR) and temporary (VVR and NVR). The accounting records do not reflect the differences themselves, but the amount of tax calculated on these differences.

Accounting for income tax calculations is carried out using the following balance sheet accounts:

- 09 “Deferred tax assets”;

- 77 “Deferred tax liabilities”;

- 68.04 “Income tax”;

- 68.04.1 “Calculations with the budget”;

- 68.04.2 “Calculation of income tax;

- 99 "Profits and losses",

- 99.02.1 “Conditional income tax expense”;

- 99.02.2 “Conditional income for income tax”;

- 99.02.3 “Permanent tax liability”;

- 99.02.4 “Recalculation of deferred tax liabilities and assets”

Income tax in the program: 1C: Accounting 3.0

Let's select an organization in the 1C: Accounting 3.0 program and go to setting up accounting policies:

Check the box - PBU 18/0 is used 2, if there is none.

Let's go to the information register Income tax rate and set the values. It should be remembered that rates may differ for different regions of the Russian Federation.

Before viewing the relevant income tax reports, it is necessary to perform a regulatory operation - Closing the month. Then you can move on to reports.

For internal analysis there is a report - Analysis of the income tax situation, where you can always select the section you are interested in.

There is also a report Certificate of income tax calculation, in which it is convenient to analyze the obtained data.

A report intended for submission to the tax office - Income tax return. This report can be accessed through 1C-Reporting.

Income tax in the program: 1C:UPP 1.3

In the 1C:UPP 1.3 program there is a document - Income tax calculation

This document performs routine tax accounting operations to obtain information on income tax. The document is entered after all routine accounting and tax accounting operations have been completed. Each organization has its own separate document.

After which you can use the reports specified in the previous section (for the Accounting 3.0 configuration)

Income tax in the program: 1C: ERP. Enterprise Management 2.0

In the 1C program: ERP Enterprise management 2.0 for the formation of income tax there is a document - Regulatory operation. To generate income tax, you need to create the specified document with the type of operation -Calculation of income tax.

The Scheduled Operation document will generate the following transactions:

After which you can go to Regulated reporting and generate an income tax return for the desired organization.

Thank you!

Golovin Pavel, author of the project “1c-nalog.info – Tax accounting in 1C. VAT, Income Tax and PBU 18",

accounting automation consultant, certified 1C-Specialist,

author of the courses “Income Tax, PBU 18 in 1C in Practice”,

“Production accounting in 1C-UPP for managers.”

Working with the report “Analysis of the state of tax accounting for income tax”

In all 1C configurations that have accounting and tax accounting blocks (1C-Accounting, 1C-Complex Automation, 1C-UPP), there is a report “Analysis of the state of tax accounting for income tax”.

The report is intended to check the turnover of income and expenses taken into account when calculating the tax base for income tax according to accounting and tax accounting data, taking into account temporary and permanent differences.

The report is not intended:

- to analyze data on income and expenses related to activities subject to UTII, with the exception of those expenses that are assigned to activities subject to UTII as a result of distribution based on income received.

- to analyze income not taken into account when determining the tax base.

The analysis is carried out by comparing accounting data, tax accounting and accounting for permanent and temporary differences. Data comparison is based on equality in rpm corresponding accounts by type of accounting:

BU = NU ± PR ± VR

(I use the “±” sign to emphasize that the accounting and accounting amounts must be positive with the exception of reversal operations, and the amount of differences can have both a “+” and “-“ sign).

1c Report Analysis of income tax

Using the structure of the tax base, you can go to the accounting section of interest. The transition from one scheme to another is made by double-clicking the mouse on the block with the indicators of interest.

If you select the “Tax” section, the diagram “ Income tax calculation»

In the diagram, the analysis is carried out by comparing the amount of income tax according to tax accounting data (income tax return) and according to accounting data, taking into account the recognition and write-off of permanent and deferred tax assets and liabilities (income statement).

If the amount of income tax according to accounting data coincides with the amount of income tax according to tax accounting data, then tax accounting is regarded as correct. The exception is when there is an accounting loss during the audited period.

In this case, in the diagram, the blocks “Income tax according to NU data” and “Income tax according to accounting data, taking into account adjustments” are circled green frame.

Each block of the scheme has a name and 4 amounts, according to the types of accounting - BU, NU, VR and PR

By selecting a block in the diagram for decoding (for example, Income), a more detailed diagram for the selected block opens

If there is no detailed diagram for the block, then a report is opened on the summary transactions (turnovers) that formed the indicators of the block.

Below is an example of decoding the “Revenue from ordinary activities” block.

By setting the “Expand by documents” flag, the report expands to the primary documents that generated the indicators.

Any document included in the report can be opened by double-clicking on the selected line.

Thus, by sequentially moving from block to block and deciphering the indicators, you can reach the primary documents,

If the indicators of any block do not satisfy equality

BU = NU + PR + VR, then such a block is surrounded by a red frame, which indicates the presence of an error.

By double-clicking on such a block, we get a breakdown by revolutions. By setting the “Expand by documents” and “Show only errors” flags, we detail the decoding to the documents that generated the discrepancies.

After eliminating all errors and repeating routine operations, the report should not contain blocks highlighted with a red frame:

P.S. There are situations when the income tax calculation is correct, but the blocks are still highlighted with a red frame.

There are also situations when the tax is calculated incorrectly, and there are no blocks highlighted in red.

These features of the report were explained in video appendix to the seminar “Income tax return in 1C - without errors and on time”, which was held in December.

P.S. The absence of discrepancies in the verified equality BU = NU + BP + PR indicates the first formal check for correctness. The correctness of the reflection of income and expenses for accounting and tax accounting is determined by the correct execution of primary documents and the selection of appropriate expense items.

The calculation of income tax in 1C is fully automated. There are two stages in this process:

- generation of tax accounting entries online, that is, simultaneously with accounting entries when posting primary documents;

- performing the final settlement at the end of the month when carrying out a special routine operation.

Let's look at a small example in which we will analyze the formation of the tax base and perform tax calculations.

Let's assume that the company Pioneer LLC is engaged in the production and sale of products. The production process requires purchasing materials, equipment, and paying salaries to employees. The difference between income from sales of products and costs incurred will form the basis for calculating income tax.

Let's see what transactions were formed during the execution of this document (Fig. 3). The figure shows two groups of transactions – accounting and tax. In the group of tax transactions there are three lines at once - for the amount for tax accounting (TA) and for the amounts of permanent and temporary differences (PR and TD).

In our version, no differences are formed, so the lines are empty. But in other cases, the differences will be calculated and will take part in the formation of the tax base. 1C is programmed to calculate all amounts, as well as control the main formula:

BU = NU + PR + VR

It is worth paying attention to one more important point. The amount of 5400 for tax accounting is displayed only in the “Ct Amount” column. The fact is that VAT accounts are not included in the list of tax accounts, so one-sided tax transactions arise.

Since all the nuances of forming tax accounting amounts are already included in the calculation algorithms, the user does not have to worry about the correctness and completeness of the data. All that remains is to observe the actions of the 1C program.

Receipt and acceptance of fixed assets for accounting

Let's move on to the next document. In January the enterprise (Fig. 4).

Of interest is the document on which the machine is used (Fig. 5).

To reduce tax payments, we use the right to bonus depreciation (Fig. 6).

In 1C, the depreciation bonus is taken into account in a special account KV (Fig. 7).

We will see later how exactly the use of bonus depreciation will reduce the tax.

Get 267 video lessons on 1C for free:

Reflection of wages in expenses

In the meantime, let’s take into account another type of expense – labor costs. To do this, we will create a document “ ” (Fig. 8).

When conducting, both accounting and tax entries are also generated (Fig. 9).

Write-off of materials for production and release of products

In the entries we see the amounts for both accounting and tax accounting (Fig. 11).

It remains to reflect the production and sales of products.

Figure 12 shows the transactions generated by the document "". The main thing to remember is that the amount in the transactions depends on the planned price set in advance and has no direct connection with actual expenses.

The last document in our chain – “” – reflects the sale of all manufactured products (Fig. 13) and forms our income.

So, all planned expenses and income have been taken into account. You can start calculating your income tax. This is the second and final stage of tax calculation in 1C.

Depreciation

We will complete the closing in three months – January, February and March. In February (Fig. 14), that is, next after the equipment is accepted for accounting, operations will be carried out to account for the depreciation bonus.

Figure 15 shows depreciation entries. The depreciation bonus “edited” the depreciation amount for tax accounting, resulting in temporary differences.

Calculation of income tax in 1C

The following figure (Fig. 16) shows a calculation certificate for deferred assets and liabilities, which details the calculations for their formation.

Amount 1983.33 rubles. equal to the percentage of income tax (20%) on the amount of temporary differences (9916.66).

The balance sheet (Fig. 17) contains data on deferred assets, which are reflected in account 77.

As a result, the income tax looks like this (Fig. 18):